Bull Call Spread

Risk: low

Reward: low

General Description

Entering a bull call spread entails buying calls and then selling an equal number of calls at a higher strike (same expiration month).

(draw a bull call spread risk diagram here)

The Thinking

You're bullish and are confident a stock will move up, but you think the upside is limited. You buy calls to profit from a rally, and sell higher strike calls to 1) help pay for the long calls and 2) to lower your risk (your breakeven is more favorable and your max loss potential is lower). If the stock rallies, preferably above the upper strike, you'll profit.

Example

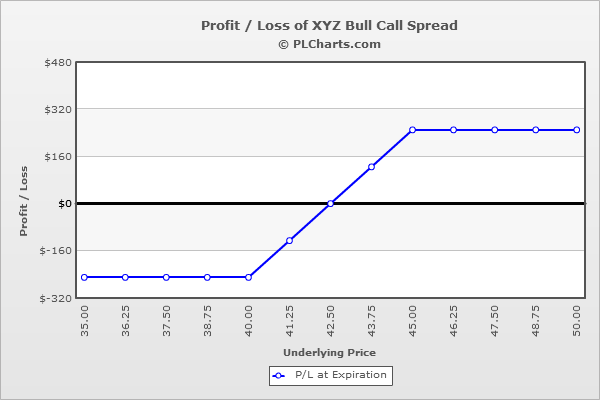

XYZ is at $42. You are bullish and think the stock can rally a few points but don't think it will surge higher. You buy (1) 40 call for $3.50 and sell (1) 45 call for $1.00. The net debit is $2.50.

Below $40, all the calls expire worthless, and your loss is the net debit paid when the trade was initiated.

If the stock trades flat and closes at $42, the 40 calls will have decreased in value from $3.50 to $2.00 ($1.50 loss) and the 45 calls will have decreased in value from $1.00 to being worthless ($1.00 profit) for a total loss of $0.50.

If the stock rallies to $45, the 40 calls will have increased in value from $3.50 to $5.00 ($1.50 profit) and the 45 calls will have decreased in value from $1.00 to being worthless ($1.00 profit) for a total profit of $2.50.

Above $45, the profit from the long call and loss from the short call cancel each other out.

Selling the upper strike call reduces your downside risk and lowers your breakeven level (compared to if you had just bought the 40 calls), but it also caps your upside potential.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|