Short Put Ladder

Risk: limited

Reward: limited but very big

General Description

Entering a short put ladder entails buying (1) lower strike put, buying (1) middle strike put and selling (1) higher strike put (same expiration month). It's essentially a bull put spread with an additional long put at a lower strike.

(draw a short put ladder risk diagram here)

The Thinking

Your analysis tells you a big move is coming, and you favor the downside. You enter a bull put spread which has limited profit potential to the upside, and then buy an extra put that has virtually unlimited profit potential to the downside (the stock can't go below 0). If the stock rallies above the highest strike, you'll profit (the gain from the bull put spread will be greater than the loss from the long put). But ideally the stock tanks, and your profit from the long put more than makes up for the loss of the bull put spread.

Example

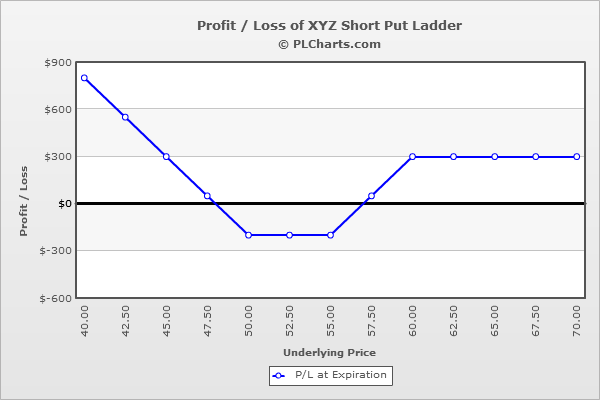

XYZ is at $55. Your research says a big move is coming, and you favor the downside because the overall market is moving in that direction. You enter a bull put spread by selling (1) 60 put for $7.00 and buying (1) 55 put for $3.00. Then you buy (1) 50 put for $1.00. The entire trade is initiated with a net credit of $3.00.

Above $60 (the highest strike), all puts expire worthless, and your profit is the net credit received when the trade was initiated.

Below $50 (the lowest strike), all puts expire in-the-money. The profit from one of your long put legs will be canceled out by the loss from your short put, and then the remaining long put will increase in value point-for-point with the stock. For example, at $45, the 60 put will be worth $15.00 ($8.00 loss), the 55 put will be worth $10.00 ($7.00 profit) and the 50 put will be worth $5.00 ($4.00 profit). The net is a $3.00 profit.

Between the two lower strikes ($50 and $55), the max loss is suffered. That’s where the profit from the short put will not be enough to offset the loss from the two long puts. For example, at $55, the 60 put will be worth $5.00 ($2.00 profit), the long puts will expire worthless ($3.00 loss on the 55, $1.00 loss on the 50). The net of this is a $2.00 loss.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|