Short Call Ratio Spread

Risk: unlimited

Reward: limited

General Description

Entering a short call ratio spread entails buying lower strike calls and selling twice as many higher strike calls (same expiration month). It can be thought of as a long call ladder, but instead of the short calls being staggered, they use the same strike. It's also similar to a call ratio spread, but the ratio of short to long calls is locked 2:1.

(draw a short call ratio spread risk diagram here)

The Thinking

Your research tells you a stock has modest upside potential but will not rally hard and will not experience a big expansion in volatility. You enter a bull call spread to profit from such movement and then double up on your naked call leg at the upper strike to help finance the spread and to lower your breakeven level.

Example

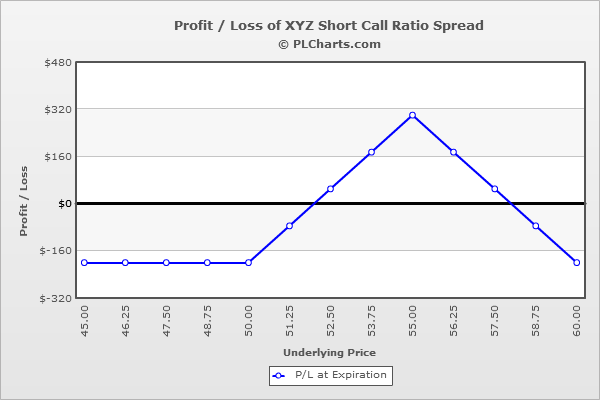

XYZ is at $52.50. You think the stock could move up a couple points but a big rally is not in the cards. You buy (1) 50 call at $5.00 and sell (2) 55 calls at $1.50. The trade is initiated for a net debit of $2.00.

Below the lowest strike, all calls expire worthless, and your profit or loss is the net credit or net debit; in this case it’s a $2.00 loss.

At $55, the short calls strike, your max profitability occurs. The 50 calls will be worth $5 (breakeven), and the 55 calls will be worthless ($1.50 gain per contract). The net of this is a $3.00 profit.

Above $55, the loss from one of the short calls will be countered by a gain from the long call, and the one remaining short call will lose you money point-for-point with the underlying. For example, at $60, the 50 call will be worth $10 ($5.00 gain), and the 55 calls will be worth $5 ($3.50 loss per contract). The net is a $2.00 loss.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|