Long Call Synthetic Straddle

Risk: limited

Reward: unlimited

General Description

Entering a long call synthetic straddle entails buying (2) calls for every 100 shares of stock you are short. The risk profile is identical to a long straddle.

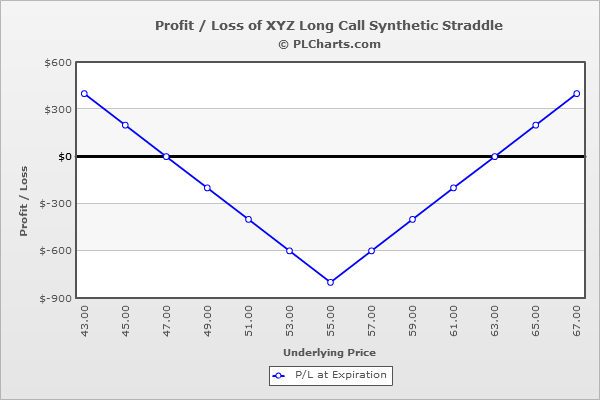

(draw a long call synthetic straddle risk diagram here)

The Thinking

You're not bullish or bearish, but you do think a big move is coming and along with it, an expansion in volatility. But you're already short the stock. Instead of employing one of the various strategies that profits from a big move in either direction (such as a long straddle), you wish to use your short stock position to synthetically mimic such a strategy. This can be done by buying calls. If the underlying drops, your short stock will net you a profit (granted it has to drop enough to compensate you for the net debit incurred by buying the calls). If the stock rallies, the gains from one of the long calls will cancel out the loss from the short stock, and the remaining long call will net you a profit (again, once the stock has moved up enough to pay for the net debit).

Example

XYZ is at $55. You short 100 shares of the stock at $55.00 and then buy (2) 55 calls at $4.00 each. The net debit is $8.00 plus the short stock.

If the stock closes at $55 on expiration day, the calls expire worthless, and you’ll lose the net debit paid to initiate the trade.

If the stock drops, you’ll make money point-for-point with the stock, but the stock will have to drop 8 points to compensate you for the total loss of the calls which will expire worthless. For example, at $45, you’ll be up $10 on the short stock, and the calls will expire worthless ($8.00 loss). The net will be a $2.00 profit.

If the stock rallies, the loss from the short stock position will be countered by a gain from one of the long calls, and the other long call will increase in value point-for-point with the underlying. But like the needed downside move, the stock has to move 8 points in-the-money before this remaining call will start making you money. For example, at $65, you’ll be down $10 on the short stock, and the calls will be worth $10 each ($6.00 profit each). The net will be a $2.00 profit.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|