Short Put Condor

Risk: limited

Reward: limited

General Description

Entering a short put condor entails selling (1) lower strike put, buying (1) middle strike put, buying (1) higher middle strike put and selling (1) higher strike put (same expiration month, distance between the two lower legs is equal to the distance between the two upper legs). It's essentially a combination of a lower strike bear put spread and a higher strike bull put spread, and it's similar to a short put butterfly except the long puts are spread out over two strikes.

(draw a short put condor risk diagram here)

The Thinking

You're not bullish or bearish, but you do think a big move is coming and along with it, an expansion in volatility. You employ a lower strike bear put spread, which achieves max profitability when the underlying drops (although profitability is capped) and a higher strike bull put spread, which achieves max profitability when the underlying rallies (although profitability is capped). If you are correct, if the stock moves big (preferably above the upper strike or below the lower strike) you'll profit.

Example

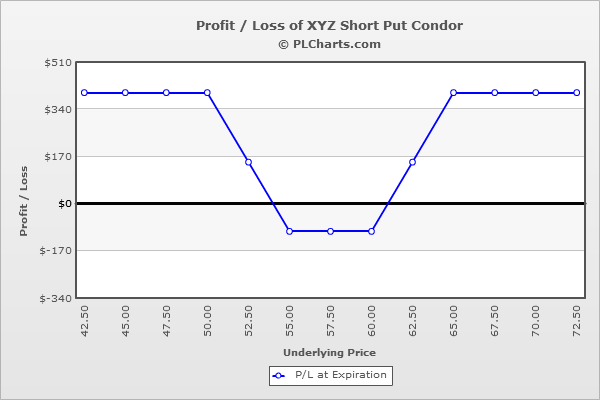

XYZ is at $57.50, and your analysis says a big move is coming (earnings or some other big announcement). You sell (1) 50 put for $0.50 and buy (1) 55 put for $1.00 to complete the bear put spread. Then you buy (1) 60 put for $3.50 and sell (1) 65 put for $8.00 to complete the bull put spread. The net credit is $4.00.

Above the highest strike, all puts are out-of-the-money and expire worthless, and your profit is the net credit received when the trade was initiated.

Below the lowest strike, all puts are in-the-money and exactly cancel each other out. Your profit is the net credit collected when the trade was initiated. For example, at $40, the 50 put will be worth $10 ($9.50 loss), the 55 put will be worth $15 ($14.00 profit), the 60 put will be worth $20.00 ($16.50 profit) and the 65 put will be worth $25.00 ($17.00 loss). The net of this is $4.00 profit.

Between the middle strikes ($55 and $60), the max loss is suffered. After all, that’s where the lower strike bear put spread and the upper strike bull put spread both are at a max loss, so it’s a double whammy. As an example, at $57.5, the 50 put will be worthless ($0.50 profit), the 55 put will be worthless ($1.00 loss), the 60 put will be worth $2.50 ($1.00 loss) and the 65 put will be worth $7.50 ($0.50 profit). The net of this is $1.00 loss.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|