Long Guts

Risk: limited

Reward: unlimited

General Description

Entering a long guts entails buying lower strike in-the-money calls and buying an equal number of higher strike in-the-money puts (same expiration date). It's similar to a long strangle, but instead of using out-of-the-money options, in-the-money options are used.

(draw a long guts risk diagram here)

The Thinking

You're not bullish or bearish, but you do think a big move is coming and along with it, an expansion in volatility. Compared to a long strangle, your net debit to initiate the trade is greater, but because the stock is already in-the-money, your breakeven levels are more favorable. If the stock rallies, hopefully it rallies enough so the profit from the long calls more than offsets the loss from the long puts. If the stock drops, hopefully it drops enough so the profit from the long puts more than offsets the loss from the long calls.

Example

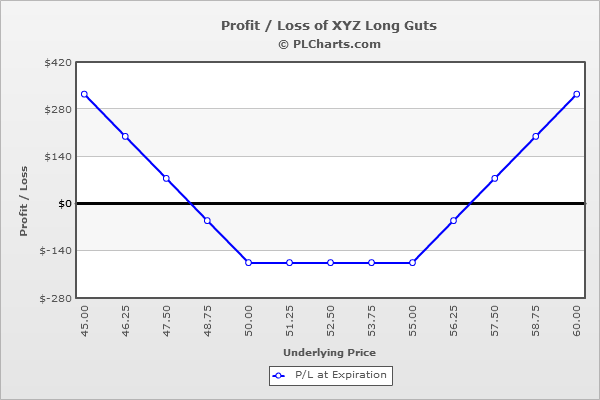

XYZ is at $52.50, and your analysis says a big move is coming (earnings or some other big announcement). You buy (1) 50 call for $3.50 and (1) 55 put for $3.25. The net debit to enter the trade is $6.75.

The underlying will have to move 6.75 points above $50 or below $55 to break even. Above $56.75, the put leg expires worthless and the call leg moves point-for-point with the underlying. Below $48.25, the call leg expires worthless and the put leg moves point-for-point with the underlying.

Because it would be impossible for both call and put to expire worthless, your max loss is not the full $6.75 paid to initiate the trade. Instead it’s a much more tolerable $1.75.

The PL chart below graphically shows where this trade will be profitable and at a loss.

|